Saving for Your Future

Understanding Compound Interest: What Savers Should Know

Compound interest is one of those concepts that sounds complicated but clicks fast once you see it in action. We put everything you need to know in one place, from the basics to the real numbers to exactly what to do next.

%20(750%20x%20750%20px).png?width=450&height=450&name=Untitled%20(750%20x%201250%20px)%20(750%20x%20750%20px).png)

What Is Compound Interest?

At its core, compound interest means you earn returns on your returns. Here's a simple way to picture it.

Imagine a snowball rolling down a hill. At the top, it's small. But as it rolls, it picks up more snow, making it bigger, so it picks up even more snow. The longer it rolls, the faster it grows. By the bottom of the hill, it's a completely different size than when it started. Your savings work the same way.

With simple interest, you only ever earn on your original deposit. With compound interest, your earnings get added back in and start earning too. Then those earnings earn. It builds on itself, over and over, every year.

Don't let the formula intimidate you! What it's really saying is that time is the most important ingredient. A small amount of money, given enough years, can grow into something much larger than you'd expect.

The Numbers That Shock People

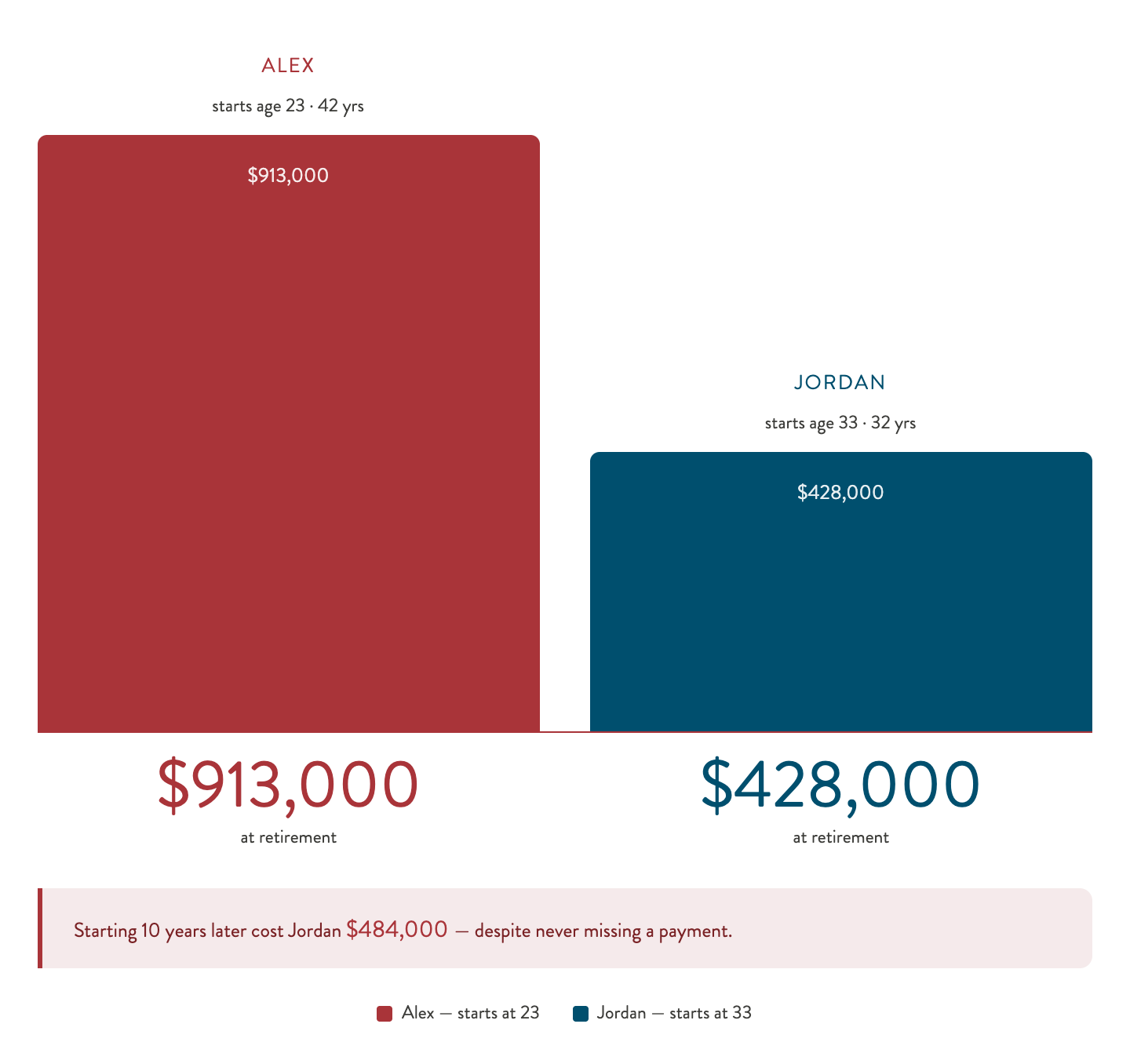

Nothing makes compound interest click quite like seeing it in concrete numbers. So let's look at two people, Alex and Jordan, who make almost identical financial decisions (keyword: almost).

The only difference is when they start: Alex starts at 23, Jordan waits until 33.

By retirement, Alex has grown their savings to over $913,000. Jordan, despite investing for 32 years and never missing a payment, finishes with around $428,000.

Nearly half a million ($484,000), just from starting earlier.

The most encouraging part of that story? Neither of them did anything extraordinary. No risky investments or financial expertise required. They showed up consistently and let compounding do the rest. The only thing that separated their outcomes was the decision to start.

That's great news, because it means the most powerful thing you can do for your financial future doesn't require a big salary or perfect budget. It just requires starting. Even small contributions, made consistently and given time to grow, can add up to something life-changing.

Wherever you are right now, starting today puts you ahead of where you'd be tomorrow.

Three Things You Can Do: Here's What Moves the Needle When It Comes to Compound Interest.

Start Small with Red Rocks Credit Union

A Reverse Tier Savings Is A Great Starting Place

Most savings accounts reward members who already have large balances. Reverse Tier Savings flips that entirely.

You earn more on your first $2,000, so your earliest dollars work the hardest for you. There’s no minimum deposit required to open the account and no service fees.

For someone younger who wants to let compounding work without needing a big chunk of money to make it worthwhile, it doesn't get much easier than this. Put in what you can, earn a strong rate from the start, and add more as life allows.

Ready to take the first step?